Are you fed up with the banks using your hard earned cash to fund the climate crisis? Ready to bank your money on a more environmentally friendly bank account instead?

Let’s be straight: I am no financial adviser. I’m a 38-year-old English writer and mum-of-one with an average ability to manage my money wisely and minimal commitment to change my financial habits (because it’s ‘too hard’ ‘takes too long’, ‘I’d rather drink wine’ etc, etc.).

But I realise — as I watch countless news reports on the Australian bushfires, floods in the UK and the world’s creeping loss of biodiversity — that I can no longer sit idly by as my money is invested in fossil fuels if I want to be the environmental campaigner I claim to be.

Scientists say we need to keep fossil fuels firmly in the ground if we are to avert irreparable damage to our planetary ecosystem. But so many banks continue to finance new fossil fuel projects. So no more banking badly. I need to invest more wisely if I genuinely care for the climate.

What follows is the late-night research I’ve pulled together to help ensure my paycheck – and yours – works to help the environment, not kill it.

Is my bank funding climate change?

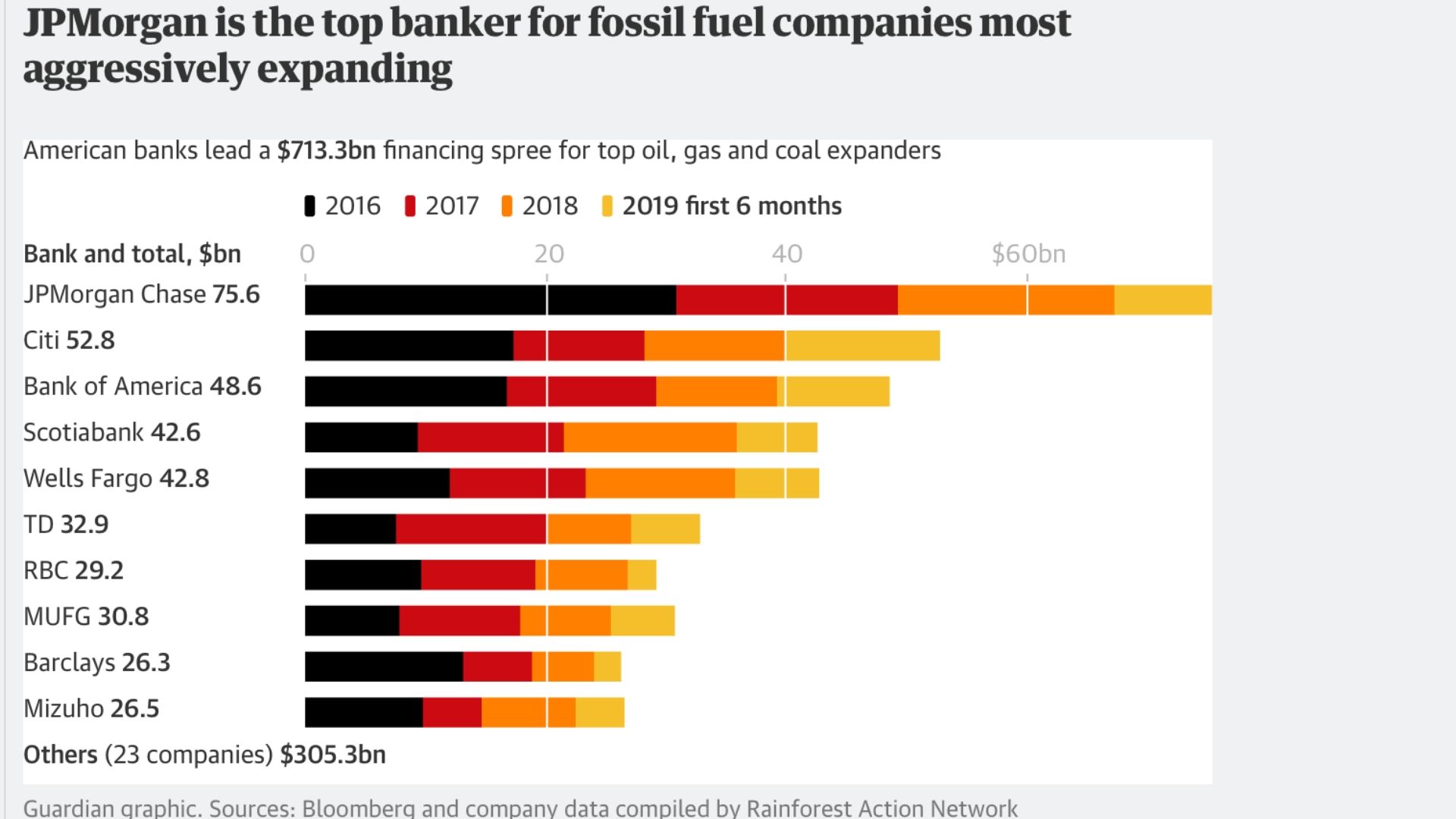

Since 2016, UK banks have poured almost £150bn into fossil fuel projects and continue to finance firms driving significant rainforest deforestation.

Highstreet banks including RBS Group (Coutts, Ulster Bank, RBS, NatWest), Barclays, Santander, HSBC and Citibank funds extreme fossil fuels, like tar sands, Arctic oil and coal mining. On the latter issue HSBC, Standard Chartered, Barclays and RBS have funded new coal plants to the tune of £25 billion since 2015. The top three banks fuelling climate change worldwide are JP Morgan Chase, Citi and Bank of America.

Was some of that wedge from your wallet?! The best thing to do is to check where your money is going. Unearthed is a good source of information as is the Rainforest Action Network, which provides a full breakdown of banks’ fossil fuel funding. Market Forces have a full list of Australian banks’.

What is the ethical alternative to high street banks?

First off, be aware the word ethical can mean several things. In finance terms it means the bank has rules and policies to ensure they have no negative impact on four key areas: the environment, animal rights, politics and human rights. I had no idea about this before I started so it’s worth researching exactly how much the bank benefits the climate if your focus is the planet – not forgetting though of course that many of those areas are intrinsically connected.

Ethical banks offer similar products and services to ordinary highstreet banks, but they vary in how they avoid supporting businesses that follow unethical practices, like supplying fossil fuels, animal testing or enabling child labour. They may invest your money in causes that have a more positive social and environmental impact, such as renewable energy sources or help for poor communities.

Which ethical banks are best for the environment?

The current account options that aren’t burdened with a load of fossils are those offered by Triodos, Nationwide and Cumberland Building Societies, Co-operative Bank and Metro Bank, according to Ethical Consumer magazine. Clydesdale/Yorkshire Bank were also listed in the report, but they are soon to go under a Virgin Money takeover.

I give a more in depth version of each of their environmental credentials below, along with a low down on which one may be better for your pocket, but before I do, it’s worth knowing the difference between building societies and banks. I didn’t know this myself before I started this research, but building societies do not invest members’ money in stocks and shares, therefore many of the issues normally associated with ethical investment do not apply to them. Banks are generally listed on the stock market and have external shareholders and usually offer a wider range of products.

Which ethical bank is better value for my money?

For anyone looking to save more ethically, it’s good to know that while the rates tend to be lower in comparison to the best deals, they are often still much better than the biggest banks, according to Your Money.com.

For example, on easy access savings accounts, ethical banks such as Triodos offer 0.80% while Ecology Building Society offers 0.85% and Nationwide (which does not make a point of supporting renewable energy, but crucially does not invest in fossil fuels) offers 0.10% to 0.25%. In comparison mainstream rival Virgin Money offers 1.5% while fossil fuelling banks HSBC and Natwest offer a meagre 0.10% – 0.25% respectively.

These ethical banks are also covered by the Financial Services Compensation Scheme, which means that up to £85,000 of your savings is protected should they go bust.

What’s more compelling is that on current accounts, ethical bank Nationwide actually comes out as best for your money compared to the dirty banks such as Santandar, according to Moneyexpert.com. Ethical banks Cumberland and Yorkshire bank are not far behind.

However, depending if you’re a student, homeowner or business owner, you’ll have different needs to consider and the rates on ethical current accounts, savings and mortgages are pretty mixed, so do your research before switching. Naturally I’d advocate you choose an environmentally-friendly bank, but we all have individual financial needs (some more great than others) so where you choose to put your money is up to you.

Here’s a quick look at those banks and building societies that have been rated highly on the environment and generally on ethical issues.

Which ethical banks are good for the environment? A summary of the banks that do not fund fossil fuels

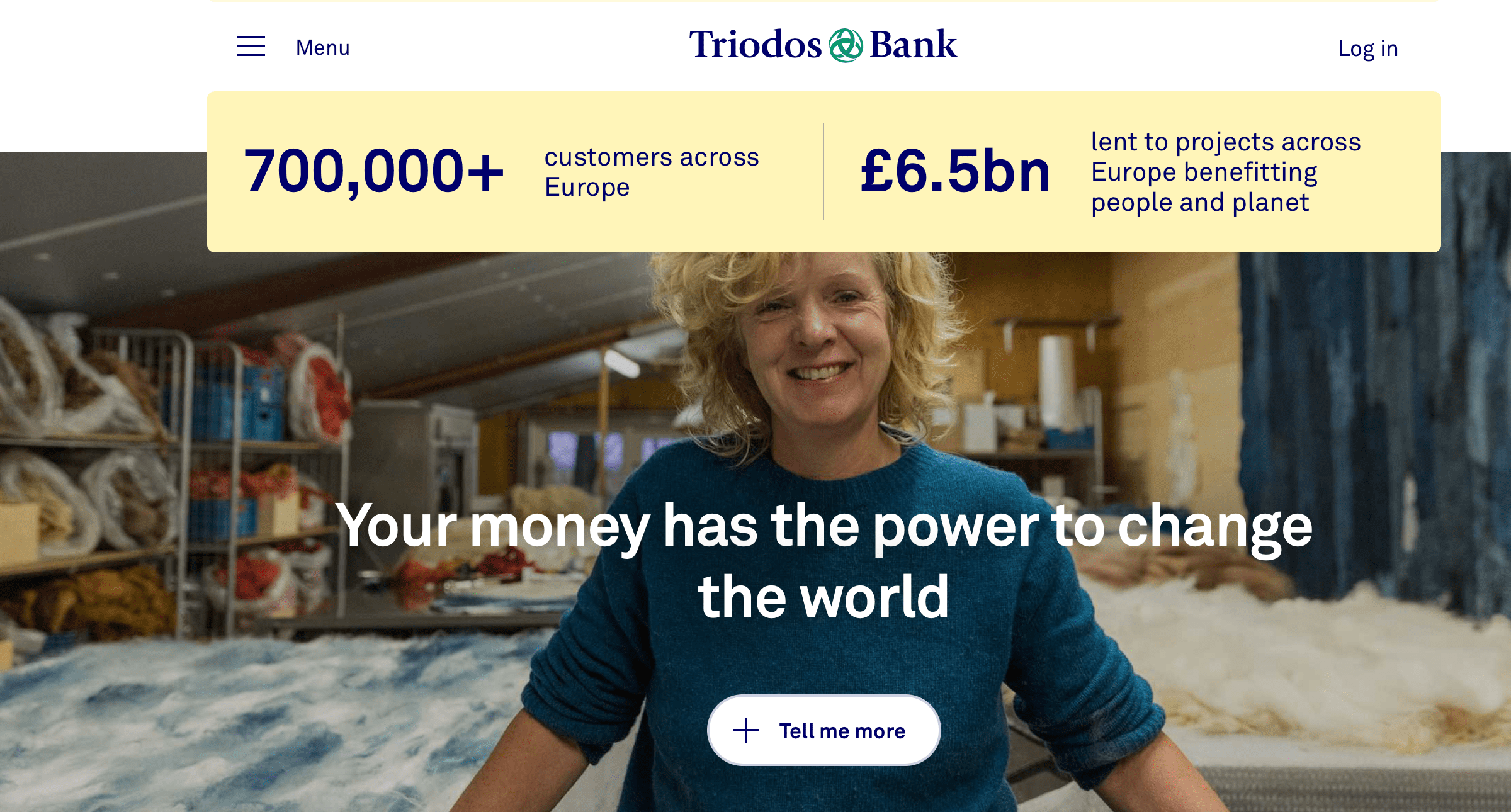

This bank is the only ethical bank that invests seriously in renewables, according to Ethical Consumer. It specialises in supporting ‘organic farming, renewable energy and ecological development to name few along with some other good causes.

It’s a bank with a difference: on its current account you have to pay a £3 monthly fee which “goes towards the cost of running your current account”, and you’ll earn zero interest on balances. But considering that banks typically fund their ‘free’ accounts with hidden costs and high charges on overdrafts; and the fact most tempting high in-credit interest rates get slashed soon after you join and this £3 charge suddenly feels very reasonable. Additionally, an overdraft facility of £2,000 is available.

The biggest benefit to this account is it’s honest and transparent. It publishes details of every organisation that it lends to on its website and claims to lend only to companies that have a positive impact on the planet. It is strikingly the most ethical bank on tax avoidance strategies, according to Ethical Consumer.

The final feather in the cap for Tridos bank is the fact that Friends of the Earth have worked with it for nearly 13 years. The charity is currently appealing to its customers to take out an account with the bank. For every new customer the bank will donate £40 to the charity once your balance reaches £100.

The Good Shopping Guide rates the Ecology Building Society second for its general ethical policies and practicals.

In terms of the climate, the building society says it is dedicated to using customers’ savings to support mortgage lending on properties and projects that respect the environment. It promises a ‘fair financial return’ for this.

The Ecology Building Society does not offer current accounts. This climate conscious bank is a good option for anyone who needs a mortgage for a property that will benefit local communities or the environment, such as someone planning to build an eco house.

If you’re after range and flexibility, then the world’s largest building society, Nationwide, probably offers the most options.

In 2016 it became the first high street financial services provider in the UK to achieve triple recertification to the Carbon Trust Standards for its “holistic approach” to managing carbon, water and waste throughout everything it does.

As a building society it doesn’t come weighed down with fossil fuel investments and claims it is ‘committed to managing our resources in ways that protect and support the long-term interests of our associates, our members and the communities in which we live and work’. Read more on their impact here.

As in independent regional building society, Cumberland claims to take its social and ethical responsibilities seriously. Its environmental policy aims to manage and reduce its environmental impacts through ‘ongoing energy conservation, recycling and waste reduction’ and as a mutual organisation it does not need to maximise profit for external shareholders, so it can afford to stick to its ethics.

This bank offers a free current account and will switch all your data over for you, so you don’t have to. It also offers a business account, savings and mortgages. You can read stories of how it benefits people in the community here.

The Co-operative bank made UK history when it publicly focussed on withholding investments from certain companies they deemed unethical or immoral. They have rejected more than £1 billion worth of loan applications since they adopted their ethical policy in 1992. The policy includes not investing in fossil fuels or arms manufacturing, or in companies that test on animals or have poor labour practices. Their refreshed ethical policy is supposedly stronger than ever.

Coop bank has suffered a difficult period – at one point their whole future was in the balance. In February 2017 the bank was put up for sale and was rescued by hedge funds, putting its ethical position under question. There’s more information on this here. However the bank has made some recovery, according to some commentators.

The bank also owns Smile, a subsidiary ethical bank.

Charity Bank comes out top of ethical banks according to Good Shopping Guide. It’s website prints full details of how much they have lent to different charitable sectors since 2002. So you can see the environment has received £10, 723, 681 compared to projects in health and social care, which received £57,184,200. Read its impact report here. It is completely owned by ‘charitable foundations, trusts and social purpose organisations’ and offers savings accounts and loans.

This new app-based bank is one of the players taking the UK under-30s by storm, mainly for the fact that it offers a prepaid debit card before switching customers over to a full-blown current account, but also because it claims to be ethical.

Credit where credit is due, it does focus on ‘solving customers’ problems, rather than selling financial products’ and it aimst to ‘get rid of punitive fees that hit when you’re most vulnerable’.

However, I couldn’t find any company information or policies about the environmental impacts of its operations. As a digital only bank it also doesn’t mention the use of data centres, which require staggeringly large amounts of carbon emissions to keep running. The rise in app-based banking is not single-handedly fuelling this, but it may be an area that the community of customers might want to ask for further information on. I also felt it would be helpful to have more information on who it’s backed by – does it include individual investors and venture capitalists who hold investments across a wide range of other industries?

Handelsbanken promote ‘responsible lending’ according to choose.co.uk. Each local branch is decentralised from the international umbrella bank, which means it gets to know its customer base and local community, ‘allowing it to make ethically sound lending decisions on a case-by-case basis’.

From an environmental point of view, the bank states that it promotes ‘sustainable investments’. It publishes a list of companies it does not work with; most of which are coal extraction companies and nuclear power companies. But the list does not include BP or Exxon, two of the world’s biggest polluters.

Since their relaunch in September 2013, TSB have made a great deal of their desire to be the UK’s ‘local bank’, in the sense that branches are independent of each other. They then take that one step further by using the money invested with them to fund loans and mortgages for other local people and businesses, according to chose.co.uk.

The modern TSB don’t have an investment banking or corporate finance arm, focusing instead on UK-only retail banking.

Do you feel inspired to change bank after reading this? Let me know by sharing your story here, by commenting below or on my Instagram page.

I found this really useful Julia. You have gathered such a wealth of information in an easy to read and understand format that making the decision to choose a bank which will provide the most ethical choice for me does not appear so daunting now. Brilliant!

Thankyou!

LikeLike